News Byte – 23.05.2026

By Byte & Block — exploring the building blocks of digital finance.

Today’s Menu

- Nasdaq Bitcoin options near launch

- Saylor adds Bitcoin sell optionality

- Europe’s euro stablecoin squeeze deepens

Nasdaq Bitcoin options near launch

Bitcoin just got another piece of grown-up market plumbing. Not flashy, not memeable, but absolutely the kind of thing that changes who can touch the asset and how much risk they can warehouse.

The SEC has approved Nasdaq’s plan to list cash-settled Bitcoin index options on the Philadelphia Stock Exchange under the QBTC ticker. These are European-style contracts tied to the Nasdaq Bitcoin Index, which tracks one one-hundredth of the CME CF Bitcoin Real Time Index and refreshes every 200 milliseconds.

The key detail is settlement. No Bitcoin delivery, no early exercise, no wallet drama. The contract turns Bitcoin exposure into something desks can model inside familiar equity-options machinery, with penny minimum price increments and a 24,000-contract position limit per side.

That is why this feels bigger than another product announcement. ETF flows already made Bitcoin demand legible; index options are the next step, turning that measured exposure into something desks can hedge, price and package.

This market read captured the practical angle: institutions do not just want spot access, they want risk tools around the exposure.

The catch: trading still needs CFTC exemptive relief. So the milestone is real, but the launch is not fully unlocked yet. That distinction matters. The market is not just waiting for more demand; it is watching the regulatory plumbing click into place one valve at a time.

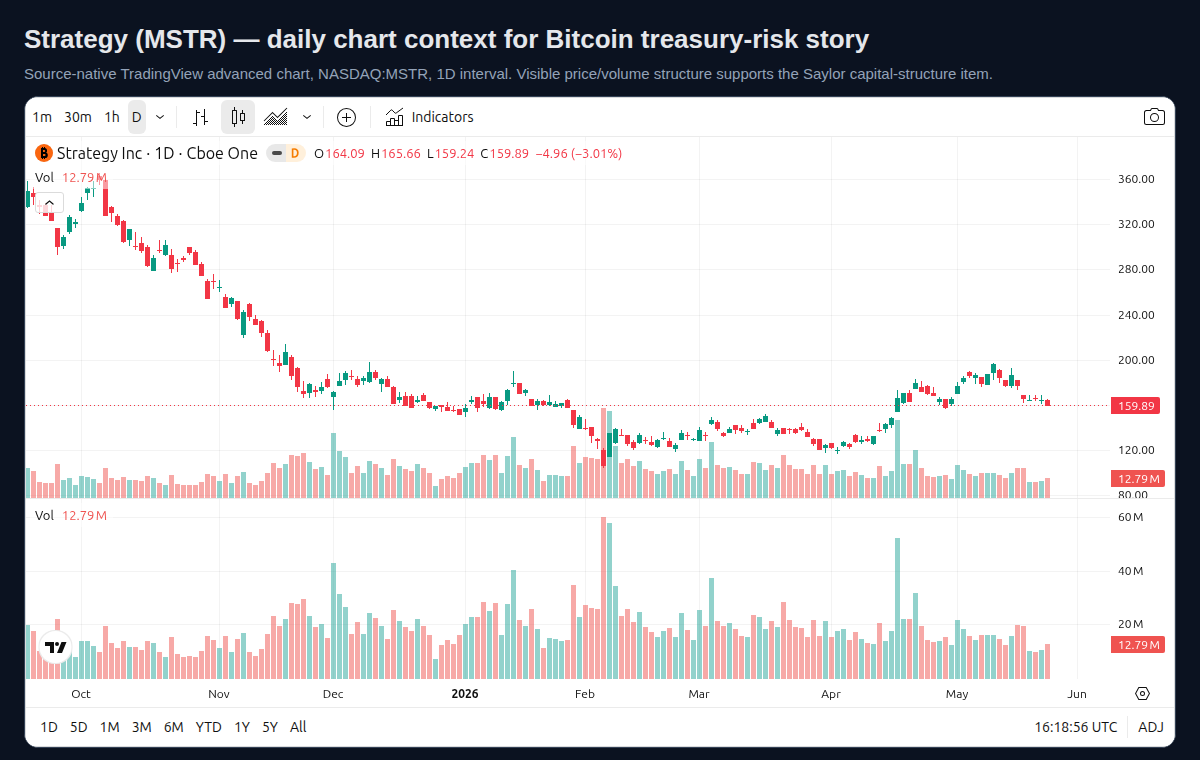

Saylor admits Bitcoin liquidity matters

Strategy’s whole Bitcoin story has always sounded cleaner when the answer was simple: buy more, never blink. The awkward update is that even the loudest Bitcoin treasury trade eventually has to speak the language of credit markets.

Michael Saylor has now opened the door to Strategy selling some Bitcoin in 2026, alongside possible equity and credit moves. That does not mean a panic sale is coming. It does mean the market is being reminded that Bitcoin-per-share magic depends on the capital stack staying trusted.

That matters because this is the same stress point we flagged when Strategy’s Bitcoin credit bet started to strain: a Bitcoin-heavy balance sheet only works if the capital machine keeps its confidence.

The numbers make the tension obvious. Strategy holds roughly 843,768 BTC acquired since 2020, with an average purchase price around $75,700. Bitcoin has been hovering close to that level, while MSTR recently closed near $159.89 after dropping about 10.86% over 30 days.

This is the uncomfortable wrapper trade in one post: the company can still be deeply bullish on Bitcoin while also needing optionality.

The important bit is not whether Strategy sells tomorrow. It is that the market can now price the possibility. Once “never sell” becomes “manage the balance sheet,” MSTR stops being a pure conviction meme and becomes a credit instrument with a Bitcoin logo on it.

Europe’s euro stablecoin squeeze deepens

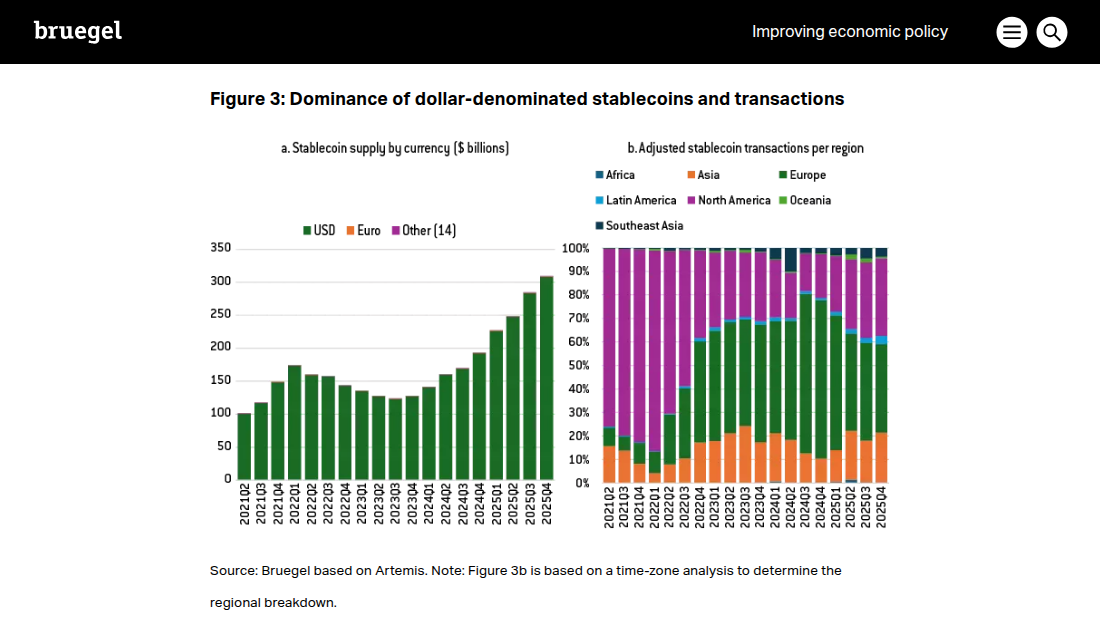

Europe wants a stronger digital-euro footprint. It also keeps looking suspiciously at the very stablecoin mechanics that could give the euro more crypto-native reach. That is the tension underneath the ECB’s latest pushback.

The central bank is resisting proposals to loosen conditions for euro stablecoin issuers, including ideas around lower liquidity requirements and possible ECB funding access. The worry is classic central-bank stuff: deposits leave banks, funding costs rise, lending weakens, and monetary policy gets harder to transmit.

The awkward part is that stablecoins were already the cleanest regulatory lane in crypto; Europe’s problem is that clarity without usable euro liquidity still leaves the dollar doing most of the work.

The gap is brutal. Europeans account for about 38% of global stablecoin transactions, but euro-denominated stablecoins represent only around 0.3% of total stablecoin supply. Circle’s EURC sits far down the global rankings, while dollar tokens remain the default settlement layer.

This post framed the policy split neatly: Europe wants less dollar dominance, but its own central bank is not eager to hand private issuers bank-like privileges.

That leaves Europe pushing tokenized finance through more central-bank-friendly rails like wholesale settlement projects, while the live stablecoin economy keeps orbiting the dollar. The policy instinct makes sense. The market outcome is still awkward: if euro stablecoins stay too small to matter, Europe gets safety, but not much influence.

Meme of the day

Follow @byte_and_block for bite-sized insights, or subscribe to the newsletter for deeper dives.

If this helped you cut through the noise, join hundreds of readers who get Byte & Block in their inbox every morning

Subscribe to our newsletter!