News Byte – 11.05.2026

By Byte & Block — exploring the building blocks of digital finance.

Today’s Menu

- Saylor’s Bitcoin credit bet strains

- XRP institutions outrun network activity

- Trump Media’s crypto losses bite

Is Saylor’s Bitcoin Credit Play Brilliant or Busted?

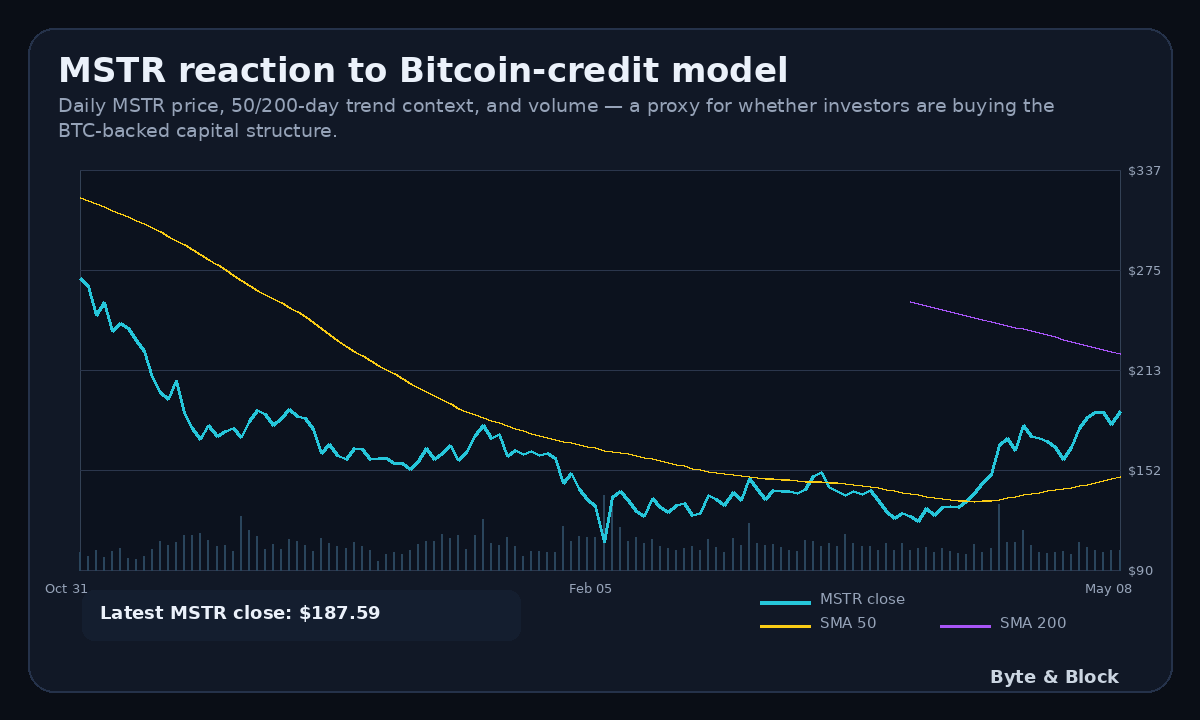

Saylor’s cleanest Bitcoin slogan just got an asterisk. For years, “never sell your Bitcoin” was the whole religion. Now the more precise version is: never be a net seller. That sounds like a tiny wording tweak, but it changes the read on Strategy’s capital machine.

The tension is STRC. Strategy says it can sell BTC if needed to fund preferred dividends, then issue enough credit to buy more Bitcoin than it sold. Saylor’s math is simple: if STRC issuance equals 2.3% of the company’s BTC holdings, the firm can pay dividends and still keep stacking. In his framing, selling one coin to support dividends is fine if the structure lets Strategy buy 30.

The real test is whether this is durable capital formation or another version of the miner problem: when the cost of capital moves against you, even a Bitcoin-heavy balance sheet can stop looking like optionality.

That is the bullish version: Bitcoin becomes digital capital, STRC becomes the credit layer, and MSTR becomes the equity wrapper around the whole machine. The bearish version is just as obvious. If the model needs asset sales, credit issuance, and constant market confidence to keep the loop attractive, critics are going to call it circular. The practical read: this is not a simple “Saylor blinked” story. It is a stress test of whether Bitcoin treasury companies can become actual credit businesses without turning the balance sheet into a vibes-powered flywheel.

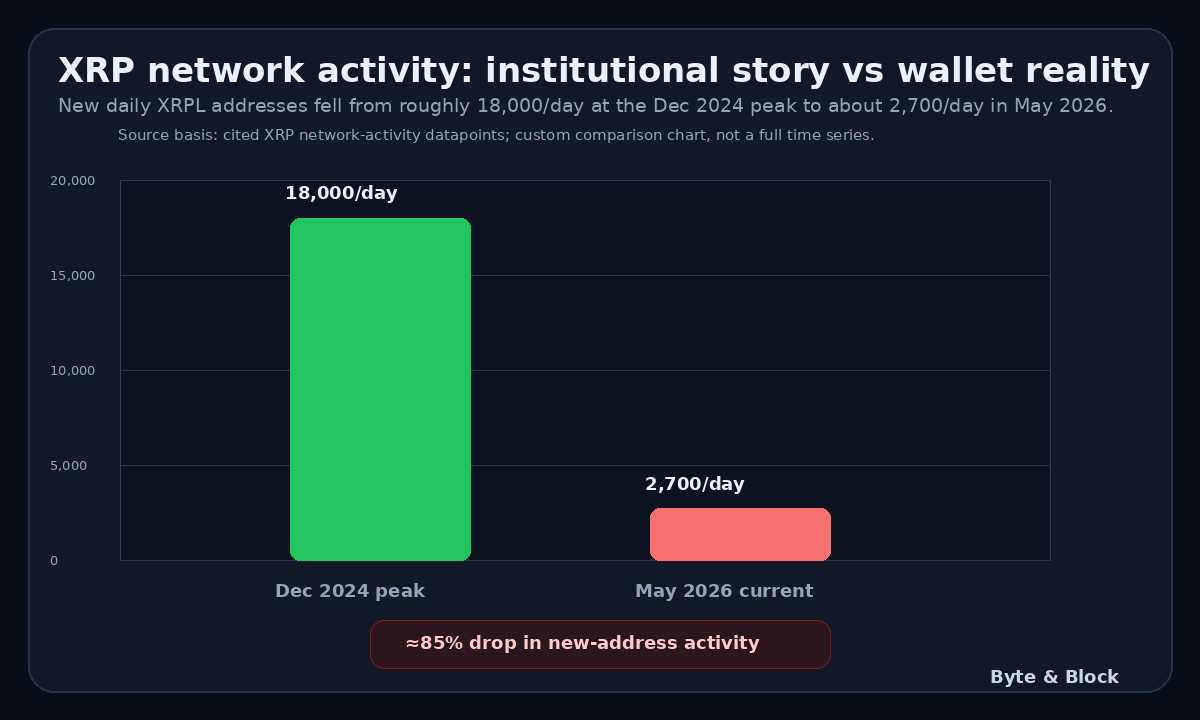

XRP Institutional Narrative vs. Network Activity Reality — Can Both Be True?

XRP has a weird split-screen problem. On one screen, institutions are finally treating it like real infrastructure. XRP ETF inflows have crossed $1.5 billion, custody balances are rising, and Ripple’s settlement story has more serious names attached than it did a cycle ago. Daily XRPL transactions even hit 3 million in March, helped by AMM pools, tokenized assets, and RLUSD settlement flows.

That is the clean bull case. The messier part is what is happening underneath. New daily addresses on the XRP Ledger have reportedly fallen by more than 80% from the late-2024 peak, dropping from around 18,000 per day to roughly 2,700. That is not the chart you expect to see if retail activity, developer momentum, and institutional utility are all pulling in the same direction.

The useful read is the same token-holder alignment problem that keeps following Ripple: company-level momentum can be real while XRP still has to prove the network is benefiting.

This does not automatically kill the XRP thesis. Institutional usage can grow before broad network activity shows up. ETFs can absorb supply without lighting up wallets. Banks can settle flows that do not look like retail speculation. But it does make the story less clean. The real question is whether XRP is becoming institutional plumbing or just getting an institutional wrapper. One supports long-term utility. The other can still pump price, but it leaves the network waiting for proof.

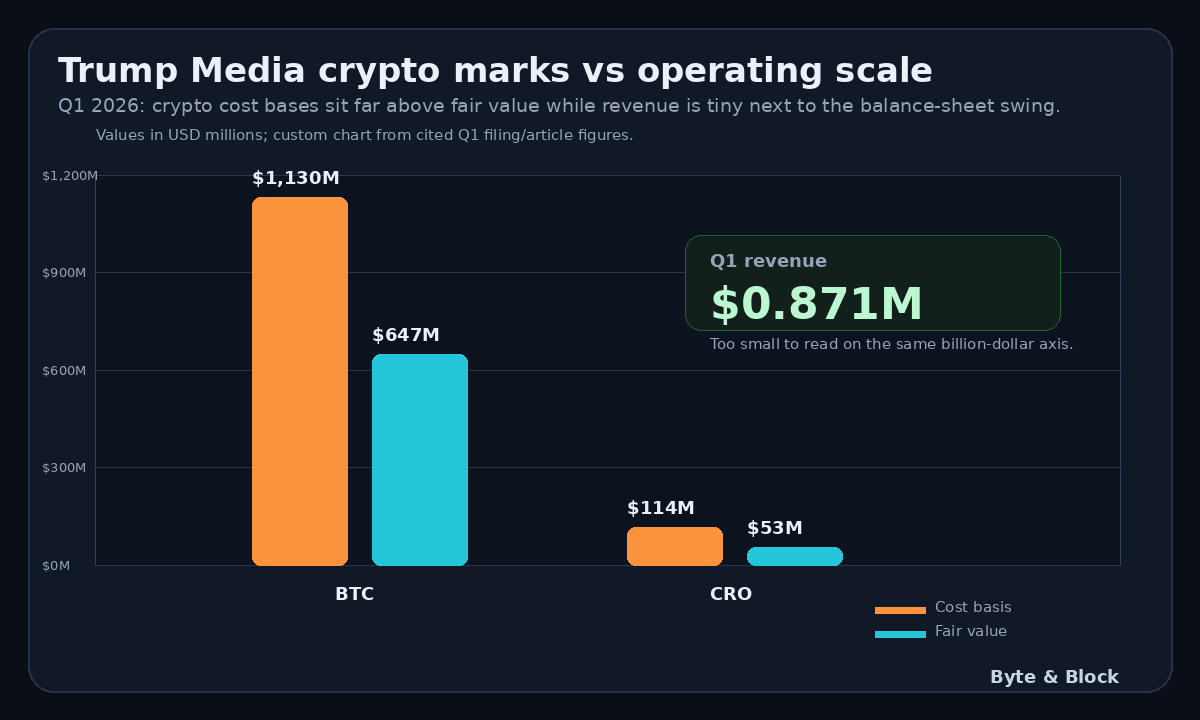

Trump Media’s Crypto Bet Is a $406M Reminder That Political Branding Doesn’t Pay Bills

Trump Media tried to wear the Bitcoin-treasury costume. The market is now checking the receipt. The company posted a $406 million net loss for Q1 2026, up from $31.7 million a year earlier. The ugly part is not just the size of the loss. It is what caused it: crypto holdings bought near the wrong part of the cycle, then marked down hard when prices moved against the balance sheet.

Trump Media held 9,542 BTC at quarter-end with a cost basis around $1.13 billion. Fair value was only about $647 million. That is the kind of gap that makes “strategic treasury allocation” sound a lot less glamorous. The company also held 756 million Cronos tokens tied to its Crypto.com deal, bought for close to $114 million and valued around $53 million by March 31.

That is what separates a treasury strategy from a balance-sheet costume: corporate crypto exposure can make sense when it supports the business case, but it gets ugly fast when the business underneath is doing less than $1 million a quarter.

The punchline is the revenue line. Truth Social’s parent generated just $871,200 in Q1 revenue. That is tiny next to the scale of the crypto-marked assets sitting on the books. This is the difference between a treasury strategy and a brand stunt. MicroStrategy at least has a coherent Bitcoin capital-markets machine. Trump Media looks more like a political media company trying to borrow crypto’s balance-sheet aura while the core business stays thin.

Meme of the day

Follow @byte_and_block for bite-sized insights, or subscribe to the newsletter for deeper dives.

If this helped you cut through the noise, join hundreds of readers who get Byte & Block in their inbox every morning

Subscribe to our newsletter!