News Byte – 07.05.2026

By Byte & Block — exploring the building blocks of digital finance.

Today’s Menu

- E*Trade pressures crypto trading fees

- Bitcoin miners split under pressure

- Bitcoin leverage crowds the $80K fight

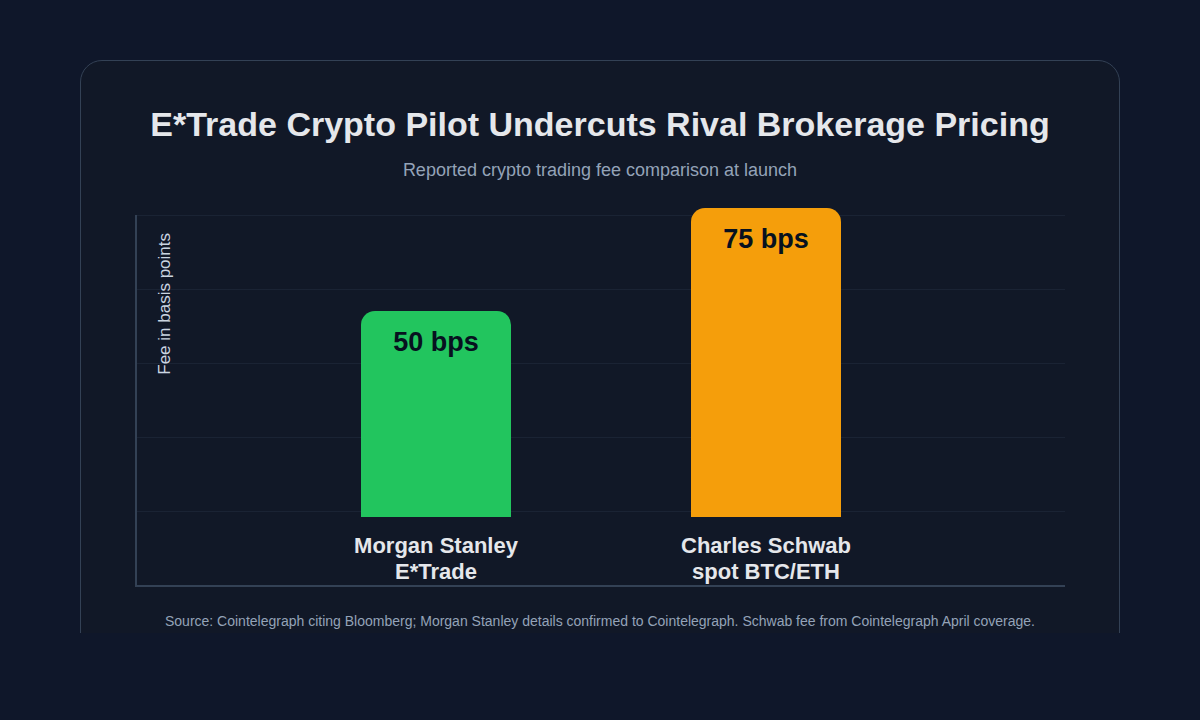

Morgan Stanley’s E*Trade Crypto Launch Is a Pricing Warning Shot at Robinhood and Cash App

Morgan Stanley is not entering retail crypto trading with a cautious “wait and see” product; it is entering with a fee signal. The planned E*Trade rollout is designed around lower crypto trading costs, with pricing aimed directly at Coinbase, Robinhood and Charles Schwab and access expected for E*Trade’s 8.6 million clients later this year.

The pilot pricing sits at 50 basis points per crypto transaction, below standard retail pricing at several major competitors. That turns the launch into more than another “Wall Street embraces crypto” headline. It makes crypto trading look like a brokerage margin-compression story.

Robinhood and Cash App have spent years making retail crypto feel native, fast and app-first. Morgan Stanley is coming from the opposite direction: a trusted brokerage relationship, a large existing client base and the ability to bundle crypto beside equities, ETFs and cash management — the same institutional wrapper that made Bitcoin demand easier to measure once ETFs arrived.

The important question is not whether E*Trade instantly becomes a crypto-native exchange. It is whether big brokerages can make basic crypto execution feel ordinary enough that users stop tolerating higher standalone fees. If Schwab, Morgan Stanley and others keep pushing down prices, crypto-native platforms may have to defend themselves with better UX, deeper asset coverage or yield-like features — not simple BTC and ETH trading spreads.

Bitcoin Mining’s Institutional Divide: Why Some Operators Flinch While Others Double Down

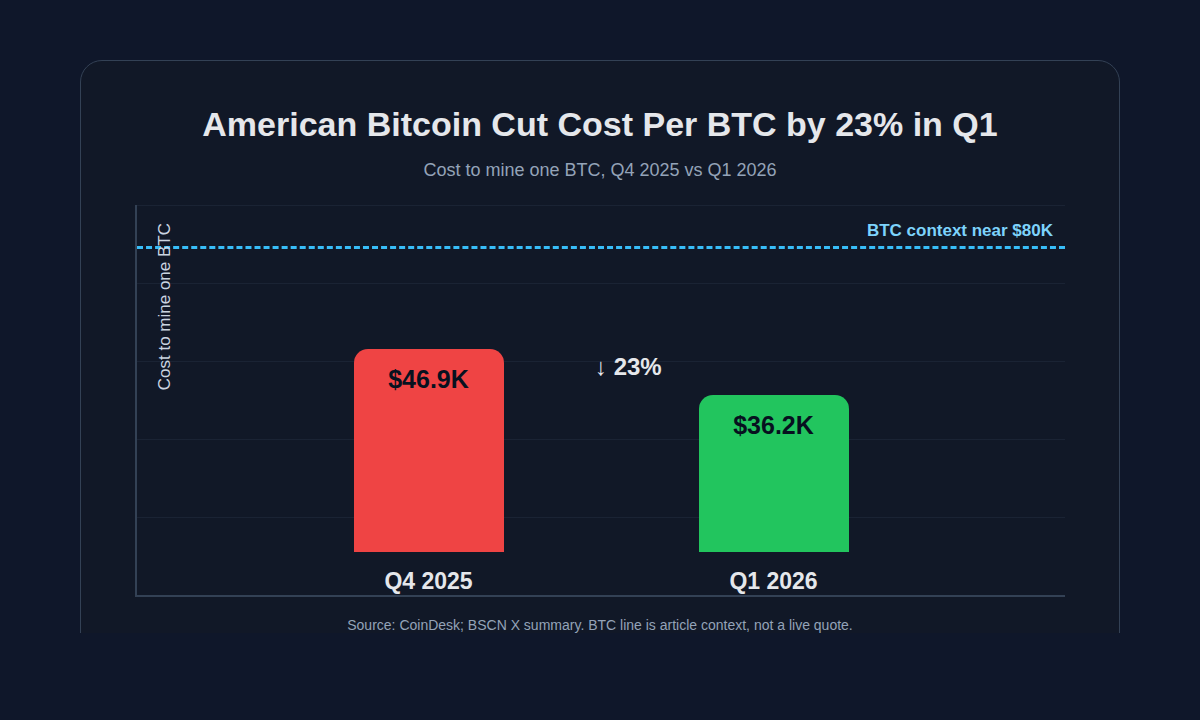

Bitcoin mining is splitting into two institutional stories: operators with cheap enough power and scale to keep accumulating, and operators forced to monetize coins or reinvent themselves. American Bitcoin sits on the first side of that divide, even though its headline quarter was messy.

The Eric Trump-linked company now reports 7,021 BTC in strategic reserves, making it the 16th-largest public Bitcoin holder, while its cost to mine dropped 23% to $36,200 per BTC despite an $81.8 million GAAP net loss. That tension is the story: earnings missed expectations, but mining costs fell sharply from $46,900 in Q4 2025 as higher production spread across a stable fixed-cost base and disciplined energy pricing.

That matters because mining stress is not evenly distributed anymore. As we’ve seen before when production costs bite, miners get pushed into decisions: hedge, borrow, dilute, sell inventory — or double down if their cost base is low enough.

A miner with a $36,200 production cost has optionality when Bitcoin is near $80,000; a higher-cost miner has a financing problem. Core Scientific shows the other path: it sold 2,385 BTC for $208.3 million in Q1 while funding an AI data-center pivot, including a major CoreWeave contract expansion. That does not mean AI pivots are wrong. It means mining is becoming a balance-sheet sorting mechanism. The winners are the operators with power contracts, capital discipline and enough margin to choose accumulation rather than forced selling.

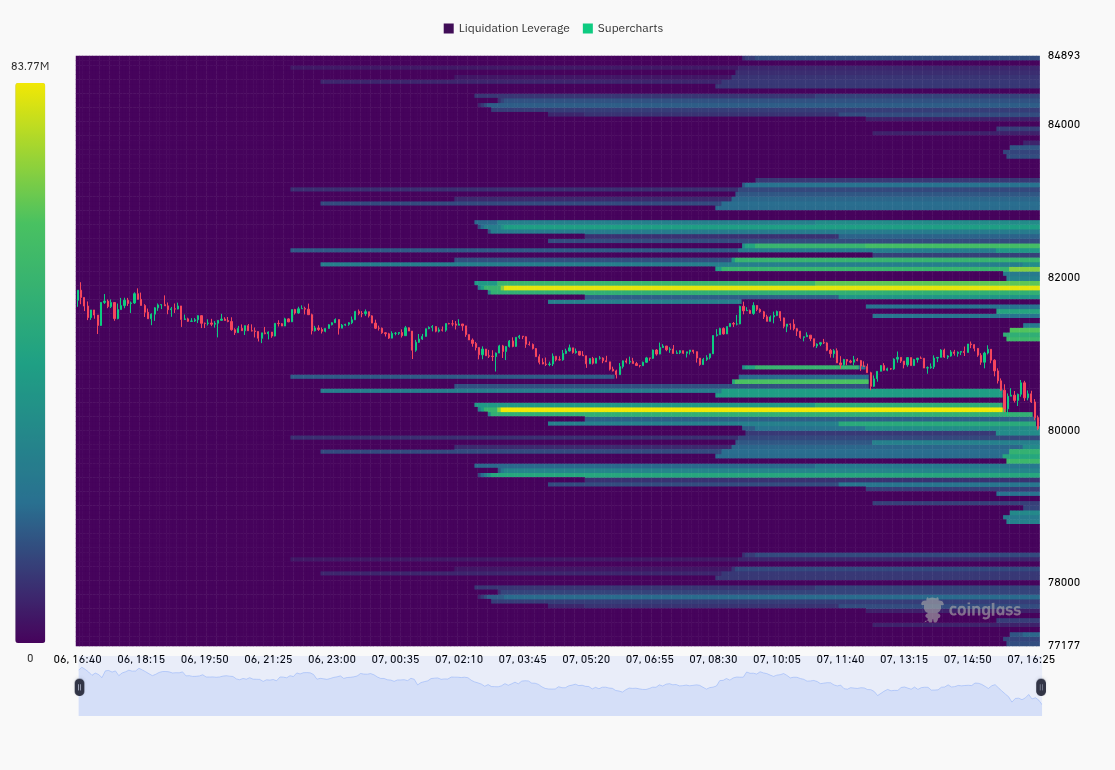

Bitcoin Traders Rejected at $80K Three Times—but Open Interest Says the Battle Isn’t Over

Bitcoin’s $80,000 level is behaving less like a clean breakout line and more like a market-structure battleground. BTC is again testing a zone that has repeatedly capped upside, with price sitting near the $80,700 short-term holder realized price — a level that can act like resistance when recent buyers are still deciding whether to hold or sell.

The spot-flow backdrop is supportive but not overwhelming. U.S. spot bitcoin ETFs pulled in roughly $2.7 billion over three weeks, yet April’s move was driven mainly by perpetual futures demand while spot demand stayed in contraction.

That is why the open-interest setup matters. This looks less like a clean breakout and more like the same kind of positioning chaos that made earlier BTC rebounds feel fragile: better flows, jumpy candles, and leverage doing too much of the work.

The near-term map looks like a liquidity squeeze: heavy short liquidations stacked around $81K–$82K, with dense long liquidity around $77K–$78K, meaning direction depends on which side gets flushed first. More than $7.9 billion in BTC shorts have been liquidated since February, while open interest has risen 6% to $29 billion. The risk cuts both ways: weak spot demand makes the rally fragile, but crowded bearish positioning can turn fragility into a squeeze if price keeps grinding into resistance over the next move.

Meme of the day

Follow @byte_and_block for bite-sized insights, or subscribe to the newsletter for deeper dives.

If this helped you cut through the noise, join hundreds of readers who get Byte & Block in their inbox every morning

Subscribe to our newsletter!